The World Has Changed

The post-pandemic landscape brought about a rapid shift in behavioral changes, driven by the adoption of more flexible work-from-home and hybrid policies. This shift has resulted in a considerable decrease in miles driven – a trend that is here to stay. The net effect – an immediate surge in popularity of usage-based and mileage-based insurance programs as policyholders demand more control over their insurance and the premiums they pay.

However, the majority of mileage-based programs in market are limited and only track actual mileage traveled – but do not factor in safe driving behaviors including distracted driving. At the same time, you and other insurers also face increased cost scrutiny during this inflationary period and hardening markets – favoring solutions that enable scale and reduce cost.

In order to drive demand for insurance products that offer greater value, build trust with policyholders, and provide rich and engaging experiences, it is essential for you to offer more personalized insurance programs and services to your policyholders.

Mileage-based insurance programs, often referred to as Pay-As-You-Drive (PAYD), are regaining traction with insurers who are looking not only to compete, but thrive, in developing innovative insurance telematics offerings in a mature market. Telematics-based mileage programs offer auto insurers a number of benefits, including:

-

Quick to implement

-

Offer more transparency

-

Provide policyholders with personalized insurance option

-

Increase policyholder retention

-

Encourage safer driver through behavior-based coaching and rewards

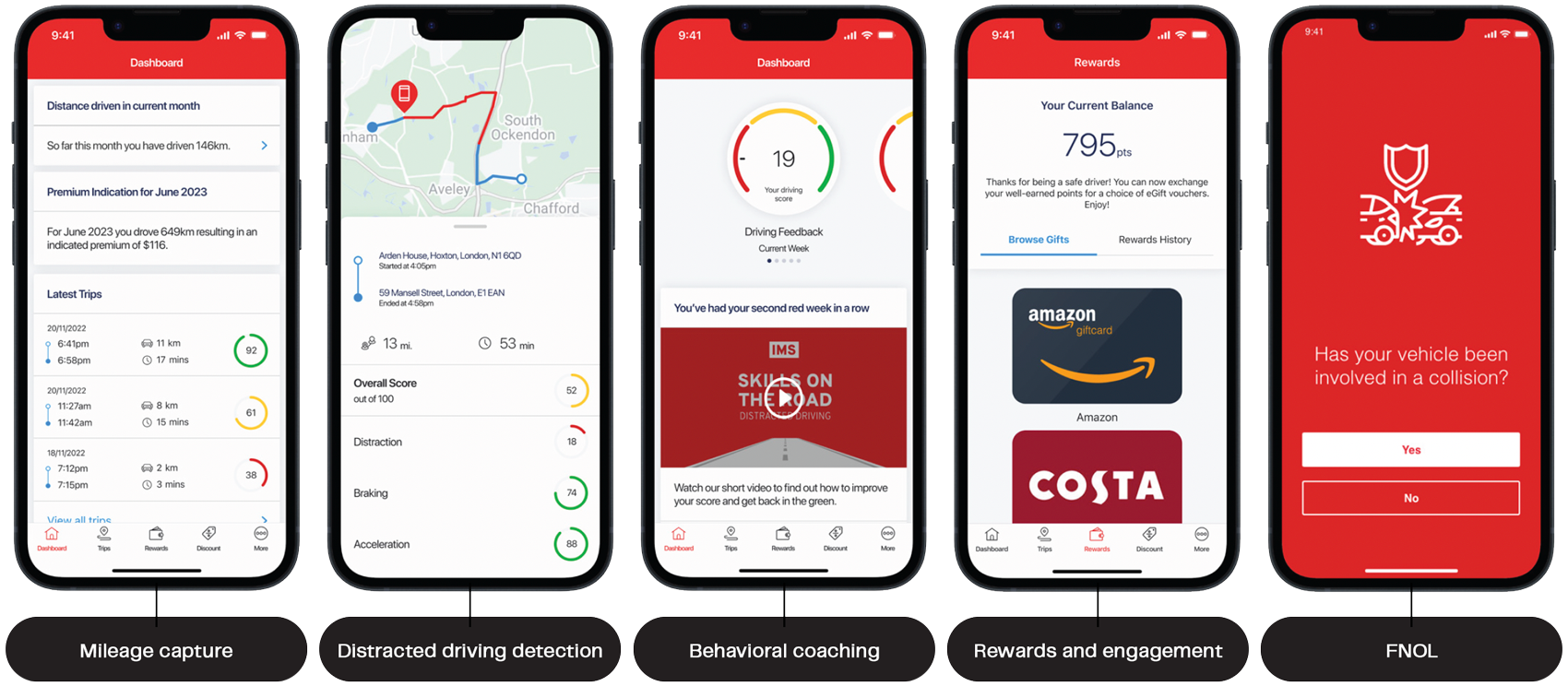

Introducing the All-New IMS Mileage UBI Offering

Only IMS provides the first mileage-based UBI product offering with a user-centric focus to enable accurate mileage capture with the added-value of engagement, including:

-

Driving behavior and distraction coaching

-

Rewards for safe driving behavior

-

FNOL/crash notification for test and learn

The IMS Mileage UBI offering provides a fully immersive policyholder experience that leverages our IMS One AppTM mobile telematics offering – the industry leading app solution for engaging policyholders proven to influence driving behavior.

The IMS Mileage UBI offering provides a fully immersive policyholder experience that leverages our IMS One AppTM mobile telematics offering – the industry leading app solution for engaging policyholders proven to influence driving behavior.

Further, to support accurate mileage capture, it provides two optional approach:

- Works with plug & play OBD-II hardware, or

- Via trip capture data provided by a third party for hardware-less approach.

Features & Benefits

Do you have the best options for your policyholders?

Features

- Full trip collection accuracy – no mileage-loss

- Frictionless experience – no Bluetooth pairing required

- Full engagement suite of optional features – coaching, rewards, right-time messaging

- App FNOL data – test & learn by correlating mileage driven to relative risk using actual claims data

Benefits

- Only UBI offering on the market proven to improve driving behavior and your claims loss ratio

- Solves profitability challenges in high premium, low mileage segment

- Offers an affordable solution for low mileage drivers – attractive option for agents to offer policyholders

- Addresses affordability challenges via policy options

- New customer acquisition – attract low mileage/low risk drivers away from competitors

Why data-driven, mileage-based insurance programs could become the ‘new norm’

Download

Comparing Smartphone, Tag, OBD, Black Box, and OEM Embedded Devices

Download

Mobile Telematics Essentials: A Fundamental Guide for Auto Insurers

Download

Nationwide SmartMiles®

Read post

MORE THAN Low Miler

Read postLearn more about IMS Mileage-Based Insurance Telematics programs

Contact us to request for more information