Automated techniques and resolving claims liability issues by introducing vehicle data captured by telematics technology as evidence of the actual events that took place, it is possible to cut days from the total automated claim settlement time. Reducing the shelf life of claims is an important factor in creating a more favorable loss ratio for insurers.

Widespread adoption of telematics data as an integral part of claims servicing has become much more common in the U.K. and Europe than in the U.S. As an example, data compiled by IMS from cases involving U.K. carriers indicated the kinds of time and cost savings that can be achieved over the claim life cycle:

- Low-speed collisions resulting in soft tissue injury show a 60 percent reduction in the claim life cycle in cases in which telematics data supports defense against injury claims. These time savings are realized by minimizing the processing and touch points for the carrier.

- For cases in which telematics data supports the defense against soft tissue injury claims, carriers can save approximately GBP £2000 [USD $2470] in legal costs, often avoiding the requirement for lengthy and costly litigation.

- In cases of mistaken identity, a common occurrence with commercial fleets, claim shelf life can be reduced by 80 percent using data to validate the alleged location of the collision compared to the tracked vehicle location.

- Use of telematics data improves efficiency in claim processing, reducing touch points by 30 percent, adding to the overall efficiency savings carriers can achieve, and reducing friction for the end customer.

Claims handlers and adjusters stand to achieve benefits both from augmented or automated processes—assisted by telematics data—in the frontline as well as the back-office, by simplifying and unifying processes that were formerly managed manually. Similarly, adjusting back-office processes with the use of telematics data (for example, verifying auto repair estimates and generating prompt reimbursements) contribute to a higher level of efficiency for claims handling.

Claims Liability and Telematics

Telematics makes it possible to determine claims liability and identify fraud because of the rich data that can be applied to visualizing and placing in context the events that took place in an accident. Although not all courts in all locales accept telematics data yet, there are many instances where information captured by telematics is being used in court to establish the circumstances of an incident and buttress or refute claims. New territories and regions continue to adapt their usage to accept telematics data as the benefits and evidentiary value becomes clearer.

Momentum is building toward increasing the use of telematics in court cases because of the significant advantages of using precise vehicle operation information captured during incidents to clarify details. For example, court cases in jurisdictions in North America and the European Union have judged the merits of claimants based on evidence provided by vehicle data captured by telematics devices. G-forces were used in some cases to indicate fraudulent accident claims occurring at a set time and place, as well as inflated claims for bodily injury. Vehicle route recordings sometimes caught fraud claims based on location data. Journey data can indicate that erratic or unsafe driving was detected before an accident occurred. In general, the number of claims cases going to court represents a very small percentage of total number of claims—the data provided by telematics can often be used effectively to settle claims before a court resolution is needed.

Experienced telematics service providers often include expert consultants who can interpret the telematics data and testify in court as to the validity of incidents when compared to the data captured by vehicle devices and sensors. Evidence of the vehicle journey, the nature of the impact events, speed and acceleration at the time of the incident, and the track record of driver behavior all contribute to providing a detailed picture of events as they unfolded.

“The market in general has taken a few years to catch up with telematics-based data analytics technology. For example, a few years back if a motor claim was disputed and telematics evidence was used, another insurer or third party solicitor would not pay much attention to this evidence. In recent years, though, this data has been playing a vital part in proving exactly what happened in an incident and building evidence towards a successful outcome for our customers.” David Johnston, Senior Claims Handler, Zurich Insurance

Essential Technology Criteria for an Effective Claims Service using Telematics

The appropriate technologies and key criteria for developing effective claims services using telematics technology and data include:

- A cost-effective, extensible telematics platform that can augment and extend your existing IT infrastructure without undue disruption of fundamental business systems.

-

Supporting sensor technology tailored to your telematics data-capture requirements and integrated into your claims processes in a responsive way. Different types of sensors have different capabilities. It’s important not to limit your selection to a single solution or a limited number of solutions. Finding a service provider that understands the tradeoffs between the various sensor technologies—self-powered Bluetooth beacons, OBD-based solutions, black boxes, OEM-embedded approaches, and smartphone solutions—makes it more likely that you can meet your exact telematics-data requirements and develop a successful program.

-

A proposition development that engages the end user and leads to improved policyholder satisfaction. A convergence of the right sensor technology, right telematics platform, a compelling engagement interaction with the end user, and a rewarding proposition can be the factors that generate better driving behavior and significant improvement in the combined operated ratio.

-

Guidance from an experienced telematics service provider (TSP) with expertise in claims services, ready to lead you through the options, tradeoffs, and requisite costs for all the solutions available in the market. The ideal TSP should also have a deep background in auto insurance claims work. The range of technologies available to support telematics, the large-scale data processing demands, and the methods for setting up and implementing effective insurance programs can be challenging to those first venturing into this market sector. Experienced guidance and a strong understanding of the technology options and their tradeoffs can help insurance firms set up and maintain telematics-based claims services confidently.

-

Expertise integrating telematics data and capture processes into existing claims operations. A high level of expertise is need to give insurers the right information and assistance to incorporate telematics data into an existing claims processing system. This goes beyond the setup and guidance expected from a typical technology company and calls for a deeper level of experience using telematics data to augment and extend a company’s claims processes to yield benefits with minimal disruption.

-

A partner organization that can train your team in the use of telematics data for combatting fraud and liability issues, optimally with experience in judicial matters involving telematics data, both history and localized trends in this area. This organization should also be equipped to represent you in court as necessary.

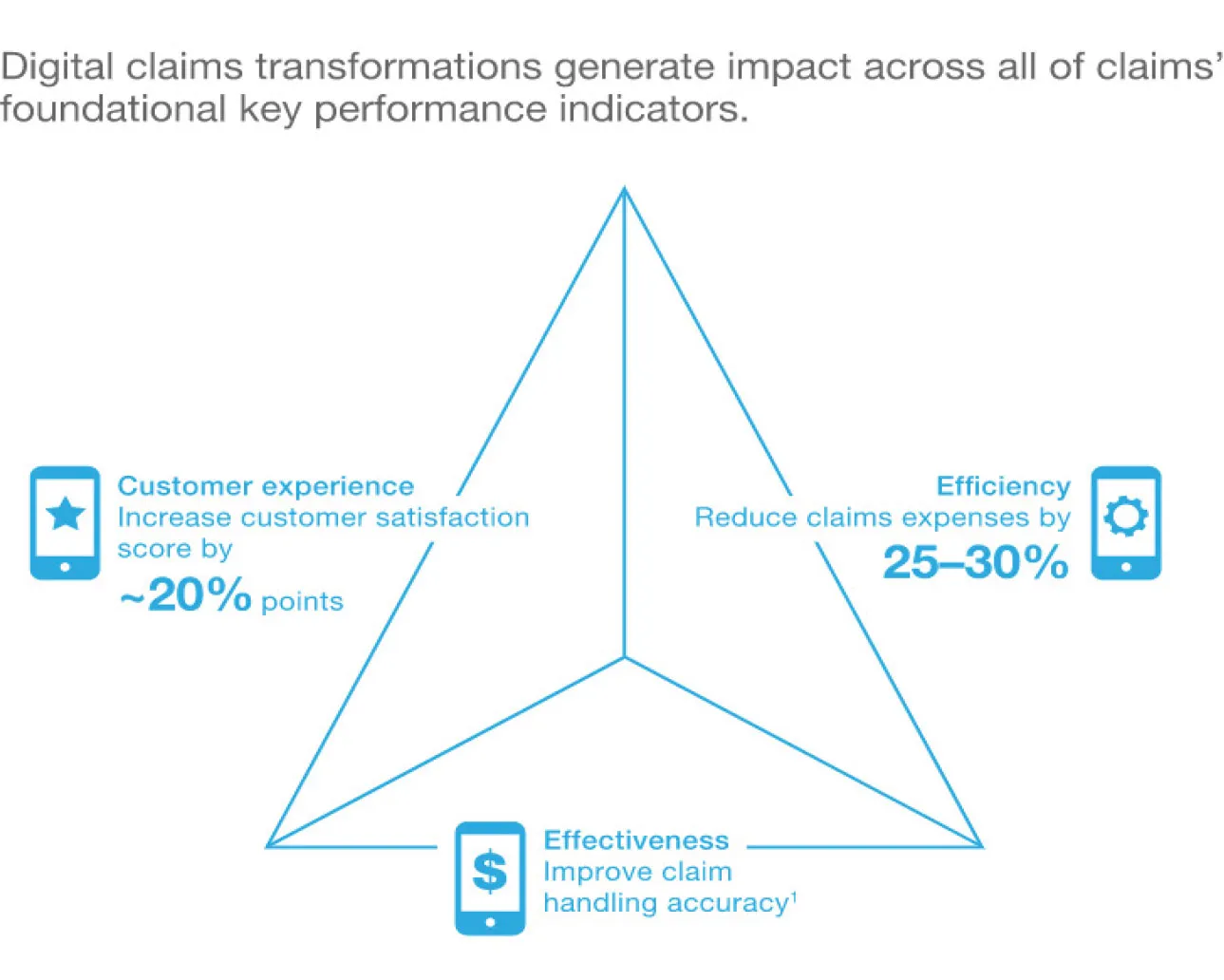

Key performance indicators show significant improvement following the implementation of telematics-based digital processes to support claims handling, as shown in Figure 2, based on information from McKinsey and Company.

With a focus on making the claims process a personalized, positive customer experience, there are many different opportunities to incorporate new tools and technologies into the automated claims services chain. These ideas are explored in more detail by EY in a document titled How to create a better claims experience.

“To effectively reinvent your business, consider carefully and then synchronize change along four major aspects of the business model—value proposition, customer base, business capabilities, and profit model. The whole organization needs to understand what investments and initiatives are needed as you tweak each element of the business model and pursue your digital future.”¹

Gartner, Speed Up Your Digital Business Transformation

Figure 1. Improvements to KPIs in response to digital claims servicing.

“As noted in our EY Global Insurance Digital Survey, the insurance industry is lagging behind other providers in developing innovative and customer-friendly digital experiences. Insurers trail the entire digital spectrum: customer engagement, use of analytics, and adoption of mobile and social media. While they have high ambitions of digital leadership, many are far from bullish about their digital maturity.” EY, The Future of Insurance in a Digital World 8

Real-World Examples and Proof Points using Telematics

Telematics and accompanying digital insurance techniques have been widely accepted in the United Kingdom and Europe, and, as a result, insurers have been able to substantially reduce claims expenses. The U.S., however, has lagged in the adoption of these technologies. Competitive pressures throughout the auto insurance sector, changing economic conditions, and the long-term prospects of work-at-home conditions are likely to alter this scenario as more and more U.S. insurers recognize the benefits of a high ROI delivered by telematics and the enhanced customer experience.

From a business perspective, transforming claims services results in clear and measurable benefits—both financial and practical—for companies that embrace this shift. The values below are expressed in both pounds sterling and US dollars for comparison, although many of studies and research projects were conducted in the U.K. because of more extensive adoption with telematics-based digital insurance strides in that territory. Some considerations for the U.S. and the rest of North American insurers as they begin transforming their claims operations:

- Positive driver behavior modification through telematics enabled programs, motivated by deeper engagement and tangible rewards, indicates that a combined COR of approximately 7.7 percent saving on claims can be achieved.

-

Research conducted by IMS reveals that as part of a comprehensive claims management program, telematics-initiated FNOL reduces claims costs by GBP £650 [USD $800] on average if action is initiated within 30 minutes of the incident.

-

A prompt response to crash incidents can also significantly lower the likelihood of fraud. Statistics compiled by the FBI reveal that insurance fraud (excluding health insurance fraud) costs the average American family USD $400 to $700 a year.⁹

-

Data accrued by IMS in working with a high-profile insurer based in Europe showed GBP £1,000,000 [USD $1,223,438] savings in claims liability costs in 2019 using telematics data as evidence.

-

Annual savings on fleet claims handling for commercial insurers, as tallied by IMS, is GBP £279,000 [USD $341,339] per 1,000 vehicles—by using telematics data.

-

Savings delivered to policyholders: The cost savings that result from smooth, reliable digital processing of telematics data can be returned to policyholders in the form of premium reductions or other benefits, providing another incentive for customer loyalty. IMS observed that policyholder retention improved significantly because of insurers lowering premiums based on their own claims savings, which were approximately GBP £900 [USD $1101] annually.

-

Quicker settlements: An effective digital approach to claims using telematics data in claims handling shortens claims processing times more than 90 percent in the case of low-speed impact claims, as well as reducing exaggerated injury claims and legal expenses. Claims life, reduced by 30 percent, also saves resource costs.

-

Reduced claims processing costs: Acquiring accident data from a telematics impact management system instead of a third party can cut claims processing costs by more than 50 percent (based on data compiled by IMS).

-

More efficient claims handling for fleet operations: Savings accrue in commercial line operations from improved efficiency, with an average annual savings of GBP £279,000 [USD $370,000] (based on IMS research).

Liability claims, especially in cases of fleet operations, can add thousands of pounds or dollars to operating costs. As acceptance of telematics data in litigation cases becomes more common, savings are likely to become substantial. Detection of fraud can be made even more compelling when data analytics and AI software are applied to the rich data supplied by telematics systems.

Increased customer loyalty through better, faster customer outcomes is a long-term benefit resulting from digital claims services based on telematics. Customers value speedy, accurate claims processing and tend to stay with insurance providers who are effective at this. Modern, automated claims processing adds to the efficiency of insurers’ daily operations and speeds response times to incidents, relying on near real-time data for quick decisions. Retaining customers is far less costly than acquiring new ones, so ensuring loyalty can be a valuable commodity for insurers.

White Paper

White Paper: Improving Claims ROI and Claims Operations with Telematics Data

Understanding Why Telematics is your Best Entry Point to Begin Your Claims Transformation Journey